Did your Parents lose 1.5 Crore?

Having covered about most of the "financial Savings instruments" in our series of blogs, We are confident that a person interested in saving his money in best way will have a clear idea about these instruments and their workings. We will now setforth to compare these to vocation out the best of them. In our last blog, we told that there is something "close to our heart" anytime and that something is "Power of Compounding". We are and will be biased towards equities because Equities are the best compounders ever in long run.

We will give away our heart by explaining how compounding works. 1 lac invested in average MF that gives 15% returns will take 5 Years to become 2 lacs, in 10 Years it will become 4 lacs & in 15 years will become Rs 8 lacs, in 20 years it will become 16 lacs. The point to be noted here is that 1 lac took 5 years to earn 1 more lac to become 2 lacs, but after 5 years, it will take only 2.5 years to earn 1 more lac. Further, after 10 Years, the same one lac will earn 75,000 every year. After 15th Year, the same one lac will earn 1.4 LAC EVERY YEAR! This is "Power of Compounding"

A lot of common men will quickly point out that 20 years is a very long time. But if thought is applied, Every savings in any form we do is for long term. Every insurance policy that is sold to us has a maturity of 15 - 25 years, the land we buy is never sold the next year or the next, it is held forever as well. The Gold we buy, the story is the same. Its time we sit back and re-think. Most of the savings we do is for our kids' education, Marriage and our retirement which is all at least 15 years away from now. Thinking long term is thinking right.

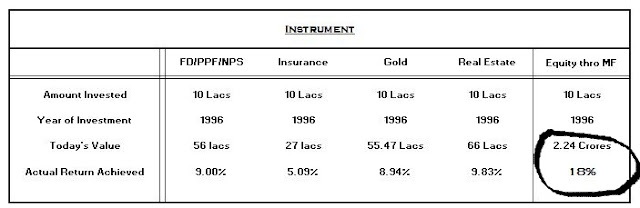

Let's get to work now. Bank Fixed Deposit, Provident Fund, National Pension Scheme, Insurance, Gold, Buying a land are the major varieties of savings we have. I will try to compare these with some examples of actual savings. Lets assume Mr A has been working for 20 Years now and started to save 4K every month since he joined his company. So he will have saved 4*12*20 = ~10 lacs so far. Lets do a analysis of Mr A would have achieved by investing in different instruments.

It is for all of us to see that by not choosing the right saving instrument, Mr A would loose approximately 1.5 crores or more. Add to this, the liquidity and the safety issues one has to face with physical asset like Gold & Real Estate. We believe that since most of our readers are still young and have time on their side, They should pause and re-think about their investment plans. With proper guidance and temperament one can achieve this without any hindrances.

We will give away our heart by explaining how compounding works. 1 lac invested in average MF that gives 15% returns will take 5 Years to become 2 lacs, in 10 Years it will become 4 lacs & in 15 years will become Rs 8 lacs, in 20 years it will become 16 lacs. The point to be noted here is that 1 lac took 5 years to earn 1 more lac to become 2 lacs, but after 5 years, it will take only 2.5 years to earn 1 more lac. Further, after 10 Years, the same one lac will earn 75,000 every year. After 15th Year, the same one lac will earn 1.4 LAC EVERY YEAR! This is "Power of Compounding"

A lot of common men will quickly point out that 20 years is a very long time. But if thought is applied, Every savings in any form we do is for long term. Every insurance policy that is sold to us has a maturity of 15 - 25 years, the land we buy is never sold the next year or the next, it is held forever as well. The Gold we buy, the story is the same. Its time we sit back and re-think. Most of the savings we do is for our kids' education, Marriage and our retirement which is all at least 15 years away from now. Thinking long term is thinking right.

Let's get to work now. Bank Fixed Deposit, Provident Fund, National Pension Scheme, Insurance, Gold, Buying a land are the major varieties of savings we have. I will try to compare these with some examples of actual savings. Lets assume Mr A has been working for 20 Years now and started to save 4K every month since he joined his company. So he will have saved 4*12*20 = ~10 lacs so far. Lets do a analysis of Mr A would have achieved by investing in different instruments.

It is for all of us to see that by not choosing the right saving instrument, Mr A would loose approximately 1.5 crores or more. Add to this, the liquidity and the safety issues one has to face with physical asset like Gold & Real Estate. We believe that since most of our readers are still young and have time on their side, They should pause and re-think about their investment plans. With proper guidance and temperament one can achieve this without any hindrances.

Below image shows the difference of PF Investment and Equity Investment of 1.5lacs every year for 21 Years.

References-

Price of Gold was 5000/10 gm in 1996 and it is 28650 at the end of 2016. Gold Prices - History

Real Estate - Price of 1 sqft of Apartment in kodambakkam was Rs1950, it is now Rs 9,500.

Equity thro MF - Aditya Birla sun Life Tax Plan.

Disclaimer - Mutual funds/Equities investments are subject to market risk!

For financial planning kindly write to us @ dropletadvisory@gmail.com

References-

Price of Gold was 5000/10 gm in 1996 and it is 28650 at the end of 2016. Gold Prices - History

Real Estate - Price of 1 sqft of Apartment in kodambakkam was Rs1950, it is now Rs 9,500.

Equity thro MF - Aditya Birla sun Life Tax Plan.

Disclaimer - Mutual funds/Equities investments are subject to market risk!

For financial planning kindly write to us @ dropletadvisory@gmail.com

Comments

Post a Comment