Did You Know - North Pole is not the coldest Place on Earth

November last year was one of the coldest months Chennai ever had in last few decades. As I cuddled in bed, sipping my hot coffee whiling away the time hopping from one social media platform to another, I came across a "Did You Know" placard.

The Placard talked about the temperatures about North & South Pole. After I read through I was boggled by the fact that the temperatures can drop so low! Oh now I know that South Pole is colder than North Pole where the temperatures can go as low as -60'C.. Then a thought stuck me - "Chennai la irukkurra 25'C ah thaanga mudilla, North Pole ah vida South Pole chillunnu iruntha namakku enna 😂" (I am not able to bear the 25'C of Chennai, what difference does it make if South Pole is colder than North!).

Now turning to the second life that I am living, that of financial advisor I started wondering that this same thought is so true to our financial lives as well. I will try to put out these in 2 scenario - Optimistic and Pessimistic.

The Pessimistic Scenario -

Wonder why pessimistic 1st? You take care of the risk, rewards will follow, that's one of the mantras for a successful financial life. When we are talking about pessimism, we are talking about risks that our financial life faces or can come across. Let's not talk about the specific risks as such because they are myriad. Let me talk about the 3 important tools namely Emergency fund/ Term Cover/Health Insurance that we will help us handle most of the financial risks in a better way. No matter how big you earn monthly and how bigger you save monthly, unless you have these 3 tools in proper place, at some point there are chances we will have to face the heat. Having these 3 tools means you are preparing your body to withstand temperatures colder than 25'C so that you can enjoy the climate rather than sulking about the cold and wrapping ourselves in a corner.

The Optimistic Scenario -

We have been writing these blogs for past 6 years and there are almost 100 blogs that we have written. Having said this, I think it is fair to be optimistic that most of our readers, if not all, will have the above mentioned tools in place to handle the financial risks in a better way. The optimistic scenario for this ilk - Starting a Saving. The biggest problem for anybody yearning to save for a future need is the Inability to Start . We are always so immersed in debts and spending for gratification that we are unable to start a saving of even 2% of our incomes consistently. Even before doing this, we start thinking about where to save? Should I do RD or put money in Sukanya Samriddhi? Should I buy a LIC Policy or do a SIP in Mutual fund? Should I invest in large cap fund or mid cap fund ? Where will I get higher return? The option that I selected is risky ? Will the option beat Inflation? or Should I simply buy a house on loan and be done with it? Or how about buying Gold? Should I buy Jewel or as coins? Should I buy as Coins or should I Invest in SGB issued by Govt ? I am so confused, so lets seek a Expert.. But hold on, Is the guy I am seeking the "Expert"? Arrey yaar! Pehle 5% Income save toh karo! (1st start saving at least 5% of your income). If you are not saving at least 5% of your income consistently (after all your loans including home loan), then these questions are like -80'C in south pole, it does not matter! You cannot withstand 25'C, 1st start preparing for this.

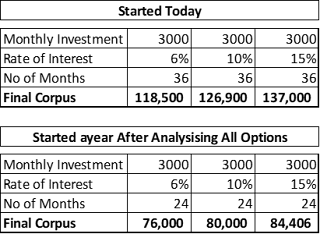

Before we wind up this piece, lets look at the simple table below -

1. In short term, it really does not matter what option you choose because the difference between lowest & highest returns is very small (~20K)

2. But If you spend time in trying to catch that 20K and delay the savings then you get almost 50% less than what you would get by starting now. More importantly one can use this 50% bigger corpus to build tools mentioned in the pessimistic scenario.

So start now!

Its important to handle the 25'C so that we can enjoy the pleasures of life without any pressures.

For financial planning and investment-related queries, write to us at dropletadvisory@gmail.com or call us at 9962399924 / 9551373455. Visit our website - www.dropletwealth.com

Good one Saravanan, keep going.

ReplyDelete